I recently had the opportunity to attend a talk given by Nicholas Hunt-Walker. Nick is a former astronomy grad student from the University of Washington, as well as an investor with one of the best trading app Ireland has, who now works as a web application developer for Starbucks HQ. During his time in academia and his transition into the tech industry, he spent a fair amount of time thinking about how to make the most out of his personal finances and how to share that knowledge with others. This article condensed version of a 90 minute long talk that he recently gave. Note: the information presented here is intended for a US audience. Some of the ideas (particularly with debt management) may not be applicable elsewhere.

Setting a Budget

For many of us, grad school is the first time in your career that you will receive a steady, regular income. Given the massive amount of new tasks and responsibilities that grad students are expected to take on, it can be dangerously easy to ignore your spending habits. Sitting down and figuring out where all of your money is going can be hard, but doing so means that you have one less thing to worry about during an already busy and stressful time in your life.

To start, you should figure out exactly how much income you receive each month. This is an important number to have in your head, as your employer can sometimes make mistakes with your paycheck that might go unnoticed (and uncorrected) unless you say something. Once you know how much money you have to work with, you should write down all of your monthly expenses that you absolutely have to pay. These include things like rent, your electricity/heating bill, and your cell phone bill.

Food, although obviously a necessity, falls into a different category. This is because food expenses are often one of the more flexible parts of your monthly budget. As a new grad student, it is easy to get consumed by work and not think ahead about cooking and meal preparation. Ordering take-out for lunch or dinner can really start to become expensive. Assuming an average meal from a restaurant costs around $12, this adds up to $720/mo if you eat out twice a day. By planning ahead, buying groceries and cooking at home, you can easily make meals that cost $5 or less. If you are in the habit of regularly eating out, this is an easy way to reduce your food expenses by 100’s of dollars each month. By far, the most effective way to reduce your spending is to cook your own food!

Although this may not be an option for everyone, finding a roommate (or roommates) and sharing rent and utility expenses is also an incredibly effective way to reduce your monthly spending. This is especially if you live in a big city, where living alone can be extremely expensive. Alternatively, housing is often cheaper away from the city center. You can often reduce your rent considerably with the tradeoff of having a longer commute.

To keep track of your spending habits and help you stick to a budget, mint.com is incredibly useful. Mint allows you to collect statements from your bank accounts and credit cards into one place and will even automatically categorize transactions for you. This allows you to quickly see how much you spend on things like groceries, restaurants or transportation. It even allows you to set a predetermined budget for spending categories and will send you an alert if you exceed this budget.

Handling Debt

Unfortunately, debt is a reality that the majority of college graduates now have to deal with, even if you do your best to budget. It is now estimated that 7 out of every 10 college graduates have some amount of student loan debt when they complete their degree (with the average borrowed amount being around $37,000). If you were lucky enough to receive subsidized federal loans, these will not accumulate interest as long as you are enrolled full-time as a graduate student (and for 6 months after). Even if you’ve managed to make it to where you are now without accumulating any significant debt, it is still important to know how to manage it. Health issues and family emergencies can come up when you least expect it, and borrowing money is sometimes your only option.

The most important piece of advice about debt management when dealing with bad credit personal loans guaranteed approval $5000 is to always try and make more than the minimum payment on loans or credit cards. The ‘minimum payment’ is simply the smallest amount than the lending company will let you pay without charging you an additional fee. The additional balance that you owe is still subject to interest, even if you make the minimum payment. The faster you can pay off the balance, the less interest you will be charged and the less money you will end up using to pay off the debt.

Sometimes, unfortunately, it is simply not possible to make the minimum (or any) payment on debt that you owe. If you find yourself in this position, the most important thing to remember is to pay yourself first. Even though it hurts to miss a payment on a loan or credit card, it is far more important to make sure your rent, utility and transportation expenses are paid first.

If you do keep missing payments on a bill or debt, the balance will eventually be transferred to a collections agency (note that this is not true for federal student loans). When this happens, your credit score will take a substantial hit. This means that the company you owe money to has decided that you are not going to pay the debt and has put it up for sale. A collections agency is a third-party company which buys unpaid debt for a fraction of its original value with the hope that you will give them something. Because the debt was purchased for less than its original value, collections companies are often willing to negotiate with you. A word of warning, however: these agencies have been known to lie and mislead. If you want to negotiate a bill that has been sent to a collections agency, it is highly recommended that you hire a credit specialist to help you. This does cost extra money, but the total cost of the specialist + resolving the debt will certainly be less than the original amount that you owed.

What to do with Extra Money

It is frighteningly easy to fritter away extra money, and if you aren’t intentionally putting it away somewhere, it will get used. Even if you are actively paying off debt, you should still be putting some of your income away, preferably into a savings or investment account. A general rule of thumb is that you should be putting away 10% of you income each month. If this is not possible, any amount is better than not saving at all.

Although it is a good idea to have an emergency fund (containing at least 3 months worth of expenses) in an easy to access place, the fact is that your money is actually losing value if you simply have funds sitting in a checking account. The reason for this is inflation. The US inflation rate has been hovering around 2% for the last decade. Unless your money is sitting in an account with at least a 2% interest rate, it is gradually becoming less valuable. The interest rate on most checking accounts (and even most savings accounts) comes nowhere near 2%. Recently, however, a number of online savings accounts have popped up with interest rates around 2%, although you should make sure that the bank you are dealing with is federally insured. These online savings accounts come at the compromise of convenience. The only way to access your money is to transfer it to another account electronically and you generally cannot make more than a few transactions per month. Most well-known banks also offer certificates of deposit (CDs) with interest rates of 2-3%, although these require you to promise that you won’t touch the money for anywhere from a few months to a few years.

Lastly and most importantly, it is never too soon to start planning for retirement. Given that social security benefits are expected to run out by 2035, it is highly likely that current 20 and 30 year olds will have to entirely self-fund their retirement. Assuming that you retire at 70 and live to 90, you will have to save 20 years worth of living expenses before that time. Fortunately, this is not quite as daunting of a task as it sounds, and it becomes easier the sooner you start working towards it. Given the meager interest rates on savings accounts, the only way that most people will be able to ever accumulate enough money for retirement is through investing.

The most common way to invest for retirement is through an investment retirement account (IRA). These are designed so that you can contribute income to them which can then be used to pay into stocks and index funds. The advantage to doing this through an IRA is that your money is not subject to many tax restrictions that you would have to deal with otherwise. The compromise here is that you cannot touch the money until retirement without incurring substantial fees.

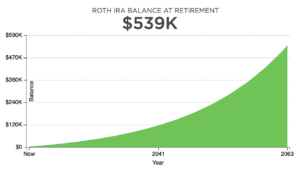

The balance of a Roth IRA account over a period of 45 years, assuming a 6% annual return rate. By contributing $200 per month, the balance in the account at retirement will be nearly $540,000. This is about 5x larger than the actual amount of money that you would need to put in.

There is a handy IRA calculator that you can use to see (roughly) how much money you will have at retirement if you start investing now. Assuming you put the same amount of money away each month until you retire at 70, you will end up with nearly twice as much money if you start at 25 rather than 35. They key point here is that when you start investing is at least as important as how much you invest. Even if you can only currently put away $10 per month, you should start now.

Finances are a subject that is often ignored and neglected early on in one’s career. The sooner you start planning for your financial future and taking control of where your money goes, the better off you will be. Grad school is already massively overwhelming. Feeling stressed and out of control of your finances, especially if you have debt to manage or family members to support, takes away from your mental well-being and makes your time in grad school feel even more difficult. Managing one’s money is a massive topic and it is impossible to sufficiently cover in an astrobites article. If you are interested in learning more about this topic, here are a number of useful links and articles:

AnnualCreditReport.com – This agency allows you to see your annual credit report and credit score for free.

How to Invest in Stocks – There are a multitude of different ways to start making money off of the stock market. This guide highlights the different paths that you can take.

Roth vs Traditional IRAs – There are two main types of retirement accounts, each of which might work better for you depending on how long you plan to invest and how much you expect to contribute in the future.

How To Manage Your NSF GRFP Fellowship – Budgeting and filing taxes can be confusing as an NSF GRFP recipient. This guide provides some useful information to help you through the process.

10 Reasons to Use a Credit Card – Credit cards have many benefits beyond allowing you to easily borrow money.

Author